Life Insurance – Imputing Income

September 2020

Download as Word.doc

Download as PDF

Introduction

Life insurance policies (both group term life and supplemental life policies) are commonly offered by employers, but such policies cannot always be provided on a tax-favored basis like group health plan coverage. Employers offering life insurance to employees and their family members need to understand the taxation rules in order to impute additional taxable compensation where appropriate. The taxation of such benefits will depend upon whose life is insured, the benefit amount, the cost of coverage, and the handling of premium payments.

Employee Life Insurance

Group Term Life Insurance

Life insurance premiums paid by the employer for group-term life insurance on the life of an employee are usually deductible as an ordinary and necessary business expense. However, premium contributions for any benefit amount above $50,000 must be taxable to the employee, whether the premiums are paid by the employer or the employee. If an employee receives a life insurance benefit amount in excess of $50,000, then the cost of the insurance in excess of $50,000, less any amount paid by the employee with after-tax contributions, should be included in the employee’s gross income for purposes of calculating social security and Medicare taxes (FICA taxes). The “cost” of group life insurance coverage in excess of $50,000 is determined using a uniform table (Table I) set forth in Treas. Reg. §1.79-3(d)(2).

TABLE I—Uniform Premiums for $1,000 of Group Term Life Insurance Protection

| Age Bracket | Monthly cost per $1,000 of coverage |

| Under 25 | $0.05 |

| 25 to 29 | $0.06 |

| 30 to 34 | $0.08 |

| 35 to 39 | $0.09 |

| 40 to 44 | $0.10 |

| 45 to 49 | $0.15 |

| 50 to 54 | $0.23 |

| 55 to 59 | $0.43 |

| 60 to 64 | $0.66 |

| 65 to 69 | $1.27 |

| 70 and above | $2.06 |

An employee’s age is determined by his or her age at the end of the taxable year.

The first $50,000 in life benefit may be handled on a tax-favored basis.

- If the premium is paid by the employer, there is no need to impute any additional taxable compensation.

- If any of the premium is paid by the employee, the employee contribution may be handled on a pre-tax basis if paid through the employer’s cafeteria plan.

For any life benefit in excess of $50,000, the value of the additional amount must be taxable to the employee.

- If the premium is paid by the employer, the employer must impute additional taxable income using Table I.

- If any of the premium is paid by the employee after-tax, the amount of imputed income is reduced by the amount of after-tax contributions made.

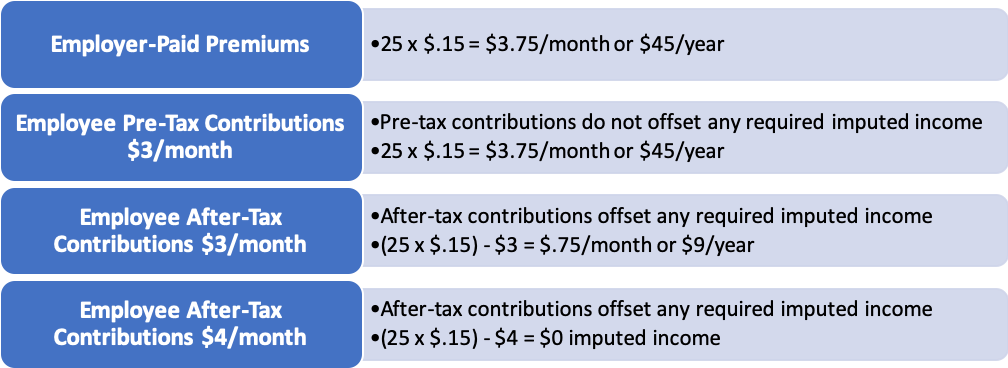

EXAMPLE: 45-year-old employee elects to receive a life insurance benefit of $75,000

Employer must impute income to the employee for $25,000 ($75,000 – $50,000)

Supplemental Life Insurance

§79 taxation rules apply to group term life insurance provided by the employer as well as any supplemental life insurance that is considered to be carried by the employer. If a supplemental life insurance policy is carried by the employer, the employer may need to impute additional taxable income to employees for the value of any insurance above $50,000 (i.e. using the Table I rates), even if the employee is paying the premiums with after-tax dollars.

A supplemental life policy is “carried by the employer” if any of the following occur:

- The benefits are provided through the same group policy as the group term life offered by the employer;

- The employer pays for any of the supplemental policy, or permits employees to pay with pre-tax dollars; or

- The rates for the group life straddle the IRS published rates in Table I (i.e. some of the life plan rates are higher than the Table I rates and some are lower).

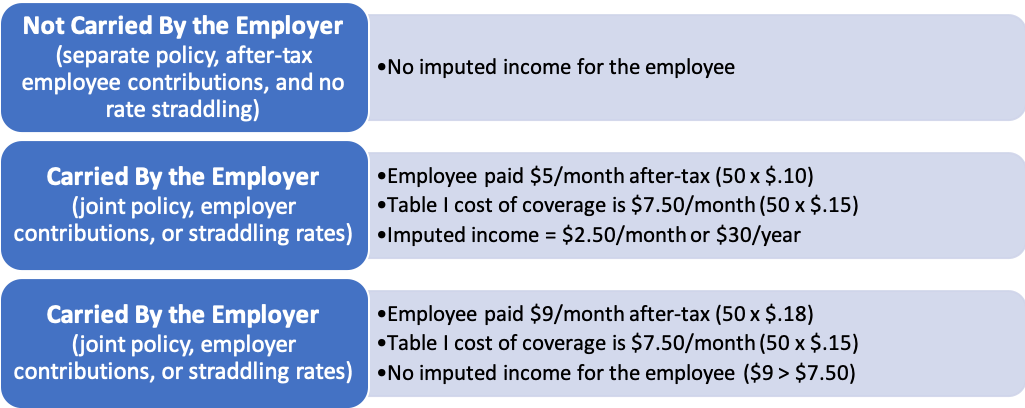

To ensure there will be no additional taxable income for employees on any supplemental life insurance purchased in excess of the $50,000 threshold, the employer should: (i) make sure that the supplemental life is provided though a separate policy; (ii) have the employee pay 100% of the premium with after-tax dollars; and (iii) ensure the monthly premium rates do not straddle the IRS table I rates. If this is the case, then there is no imputed income for the employees for any supplemental life insurance in excess of $50,000.

If the supplemental life insurance policy is under the same contract as the group term life policy, they are generally treated as one for purposes of determining taxation in accordance with §79 rules, unless there is an argument that they can be treated as separate policies. In IRS Private Letter Ruling 1350032 (https://www.irs.gov/pub/irs-wd/1350032.pdf), the IRS indicates the supplemental life policy may be treated as separate if the premiums charged are developed separately using separate actuarial computations and equal or exceed the life insurance benefit payouts for each policy year, there are no subsidies or credits exchanged between the policies, and no dividends are allocated to another policy.

If it cannot be argued that the policies are separate, the premiums are not paid 100% after-tax by employees, or the rates straddle the cost set forth in Table I, employees should have imputed income for amounts above $50,000 to the extent the premiums are lower than the rates in Table 1. However, if employees pay the premiums after-tax and the amount paid equals or exceeds the cost of coverage based on Table 1, there is no imputed income.

EXAMPLE: 45-year-old employee elects to a supplemental life insurance benefit of $50,000 (in addition to the $50,000 of group term life coverage provided by the employer)

Spousal or Dependent Life Insurance

Employer-paid dependent life coverage may be provided up to $2,000 on a tax-favored basis (considered “de minimis”), but the premium for any benefit amount above $2,000 would have to be included income similar to the process outlined above for employee life insurance above $50,000 in benefit.

Life insurance on the life of anyone other than an employee (e.g., an employee’s spouse or dependent) cannot be included in a cafeteria plan, and therefore any employee contributions toward dependent life coverage must be paid for on an after-tax basis. In addition, flex credits, if any, should not be used toward such coverage.

To avoid any need to impute income to the extent the employee payments are less than the cost of coverage as set forth in Table 1, the employer should ensure the spouse or dependent life policy is not considered to be “carrier by the employer” as described above.

While every effort has been taken in compiling this information to ensure that its contents are totally accurate, neither the publisher nor the author can accept liability for any inaccuracies or changed circumstances of any information herein or for the consequences of any reliance placed upon it. This publication is distributed on the understanding that the publisher is not engaged in rendering legal, accounting or other professional advice or services. Readers should always seek professional advice before entering into any commitments.